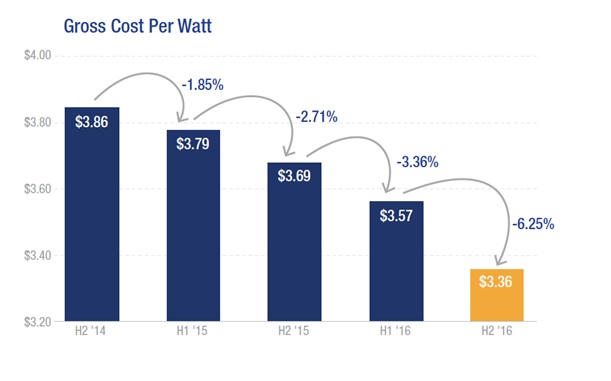

EnergySage published a new report “Solar Marketplace Intel Report,” which compared the residential PV market data in the second half of 2016 with the first half of the same year. Based on quotes EnergySage collected from market place users across 34 states and Washington DC, it revealed that the average national gross cost in H2’16 declined by 6.25% from H1’16 to $3.36.

Of the findings presented, one of particular interest is the difference in system costs among the 10 states (Arizona, California, Florida, Illinois, Maryland, Massachusetts, New York, Ohio, Texas and Virginia) EnergySage selected for this report. Looking at data in H2’16, Arizona has the lowest gross cost of $2.97/W, followed by $3.01/W in Ohio and $3.02/W in Virginia. According to the Solar Energy Industry Association, in 2016 Arizona installed 656 MW of PV, of which one thirds was for residential installations. In fact, Arizona is the second largest residential PV market. Does the low cost reflect the size of the market?

Chart: Residential PV System Cost: 1H’16 vs. 2H’16

Looking closer at the data, you will notice that California has the third highest PV system cost at $3.38, after New York with $3.59/W and Massachusetts with $3.57/W.

How does California, the biggest PV market in the U.S., have one of the highest gross costs? Isn’t this the assumption: “the more PV is installed; the cheaper installation costs become”?

A large market size does not necessarily bring down the cost

The chart below shows (1) residential PV installed system cost ($/W) in H2’16 and (2) net-metered residential PV capacity at the end of 2016 (data source: EIA).

Chart: H2’16 Residential PV System Cost and Net-Metered Residential PV Capacity (as of December 2016)

California’s residential market is about 5 times as big as that of Arizona and the cost in California is 15% higher than Arizona. Similarly, California’s residential market is about 153 times as big as Virginia, but the cost in California is 12% higher than Virginia. One would expect the market size to influence the installation costs more consistently.

Let’s check the relationship (the correlation) between (1) installed cost and (2) market size. The correlation coefficient between gross cost per watt and net-metered PV capacity is 0.32. This correlation value indicates a relatively weak positive relationship between those two variables. That means, for example, in California, the largest PV market, PV installation costs are not necessarily the cheapest.

Economies of Scale, does the size matter?

Normally, as the system size gets bigger, the cost per watt goes down. That’s why utility-scaled solar plants or non-residential PV systems are much cheaper than residential in terms of dollar per watt.

According to EenrgySage’s data, the average system size in H2’16 in Florida is 12 kW, over 70% bigger than that of California (7 kW) while the gross cost in Florida is just 10% lower than that of California. The correlation coefficient between gross cost per watt and average system size is -0.53, indicating a not-so-strong negative relationship between these two variables. It means that a larger system doesn’t necessarily lower the dollars per watt.

Chart: H2’16 Residential PV System Cost and H2’16 Average System Size

Electricity is the biggest influencer

Because utility electricity rates have a major impact on PV economics (payback time and investment return), let’s check whether electricity rates influence the system cost. The chart below shows (1) the residential PV installed system cost ($/W) in H2’16 and (2) the 2016 average residential electricity price ($/kWh) (data source: EIA).

The correlation coefficient between gross cost per watt and electricity price is 0.88, indicating a strong positive relationship between these two variables. The higher the electricity price, the higher the system cost and the lower the electricity price, the lower the system cost.

Chart: H2’16 Residential PV System Cost and 2016 Average Residential Electricity Price

Both Massachusetts ($0.19/kWh) and New York ($0.18/kWh) have the highest electricity price as well as the highest system cost. The average residential electricity price in California was $0.17/kWh. Compared to Virginia, the electricity price was 52% higher and the gross system cost was 12% higher.

Considering that component costs (solar modules, inverters and mountings) are relatively similar across the states, let’s check with an important part of the soft costs – installation labor.

By using labor data collected by U.S. Bureau of Labor Statistics, the chart below shows (1) residential PV installed system cost ($/W) in H2’16 and (2) Electricians’ (47-2111) hourly mean wage in May 2016 (data source: U.S. Bureau of Labor Statistics). The correlation coefficient between gross cost per watt and electricians’ mean hourly wage is 0.83; similar to the one with electricity price, indicating a strong positive relationship between these two variables. For example, New York has the highest electricians’ hourly mean wage as well as the highest gross cost. Virginia has the third lowest electricians’ hourly mean wage as well as the third lowest gross cost.

Chart: H2’16 Residential PV System Cost and Electricians’ Hourly Mean Wage (as of May 2016)

Looking at statewide incentive programs (excluding programs run by municipals), out of the 10 states, only Maryland and New York offer rebate programs (Maryland Residential Clean Energy Grant Program, The NY-Sun Incentive Program, respectively). Four states (Ilinois, Maryland, Massachusetts and Ohio) have active SREC markets toward the state RPS carve-out. Arizona, Massachusetts and New York offer personal tax credits.

Statewide Incentive Comparison

|

Personal Tax Credit

|

SREC Trading

(2016 Average)

|

Rebate

|

Arizona

|

25% (up to $1000)

|

|

|

Illinois

|

|

~$168/MWh

|

|

Maryland

|

|

~$167.5/MWh

|

$1000/per system

|

Massachusetts

|

15% (up to $1000)

|

~$285/MWh

|

|

New York

|

25% (up to $5000)

|

|

$0.40/W (step 7)

|

Ohio

|

|

~$15/MWh

|

|

To sum up what influences price differences among states, Nick Liberati, Communication Manager at EnergySage stated as follow:

“As far as why certain states are higher, it's most likely a result of electricity prices and the availability of incentives. MA and NY have strong incentive programs and high electricity rates, while other states (e.g., Florida, Virginia) have lower electricity rates. This means installers in these states have to price their products lower in order to be competitive, even if it means that they take a lower margin.”